Rajkot

As per RBI guidelines, the minimum down payment for a flat in India is 10–25% of the property value, depending on loan amount. Banks fund up to 90% for loans up to ₹30 lakh, 80% for ₹30–75 lakh, and 75% above ₹75 lakh. The remaining must be paid as down payment from personal funds.

One of the first questions any aspiring home buyer asks is: “How much money do I need upfront to buy a flat?” The answer is more nuanced than a simple percentage—because the down payment requirement in India depends on the loan amount, property value, lender policy, and government schemes like PMAY.

This guide by SquareYards explains RBI-mandated Loan-to-Value (LTV) ratios, how to calculate your total upfront cash requirement, and smart strategies to accumulate your down payment faster.

Understand RBI’s Loan-to-Value (LTV) Ratio Rules – The Reserve Bank of India (RBI) mandates maximum LTV ratios for home loans:

Note: These are maximums. Individual lenders may offer lower LTV based on profile.

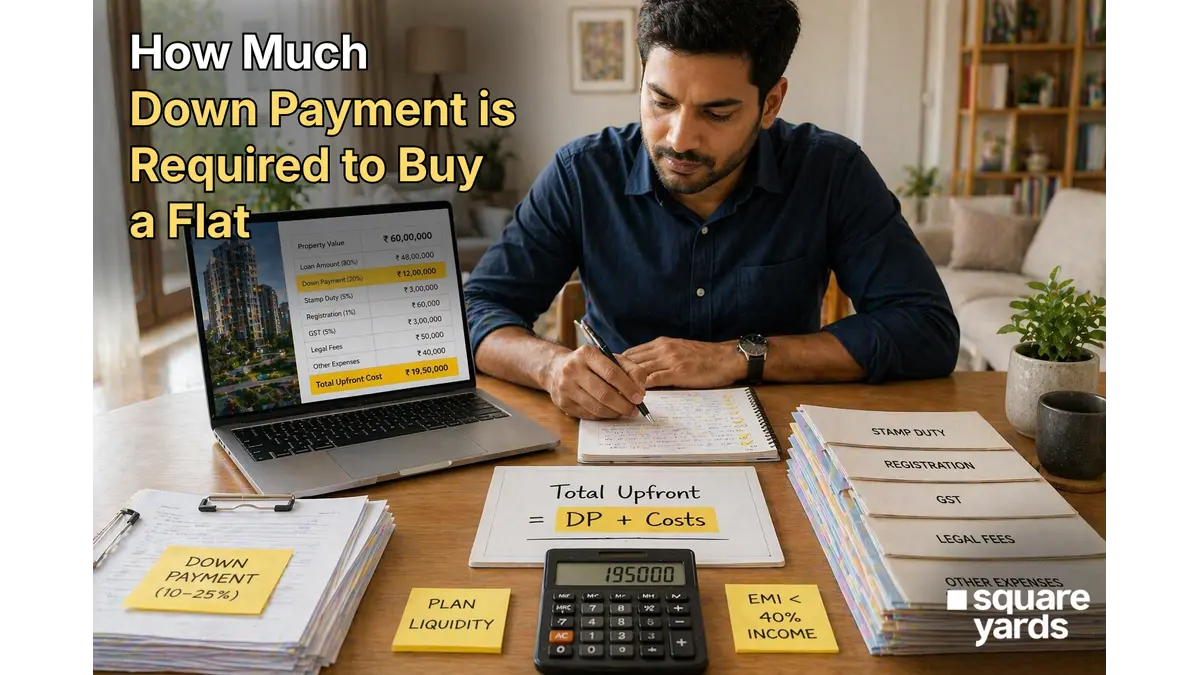

Calculate Your Total Upfront Cash Requirement – Down payment is NOT the only upfront cost. Total cash required includes:

For a ₹60L flat in Maharashtra: Down payment (20%) = ₹12L; Stamp duty (5%) = ₹3L; Registration (1%) = ₹60K; GST (5% if UC) = ₹3L; Total upfront ≈ ₹18.6L

Check PMAY Subsidy Eligibility – Under PMAY-CLSS (Credit Linked Subsidy Scheme), first-time buyers can get interest subsidies reducing effective loan cost:

This subsidy reduces your effective EMI and enables purchasing a higher-value property.

Conclusion

Understanding your exact down payment requirement is the foundation of sound home purchase planning. By combining RBI’s LTV norms, PMAY subsidies, and smart saving strategies, you can minimize your upfront cash outflow and make your dream flat a reality.

Use SquareYards’ free EMI Calculator and Home Loan Advisory service to calculate your exact down payment, loan eligibility, and monthly EMI. Explore verified flats within your budget across India’s top cities.

As per RBI norms, the minimum down payment is 10% for home loans up to ₹30 lakh, 20% for loans between ₹30–75 lakh, and 25% for loans above ₹75 lakh. However, stamp duty, registration, and other charges must be paid separately from personal funds.

Yes. EPFO allows withdrawal of up to 90% of your EPF accumulation for home purchase after completing 5 years of EPF membership. You can use this for down payment, construction, or home loan repayment. The withdrawal is partially tax-exempt under specific conditions.

PMAY-CLSS subsidy is applicable for purchase of new residential units as well as resale units, provided neither the buyer nor spouse owns any other residential property in India. The property must be in buyer’s/spouse’s name, and the loan must be from a recognized financial institution.

The booking amount is an initial payment (typically ₹50,000–₹5L) made to reserve a property. It’s part of the total down payment. The full down payment (10–25%) is paid in stages as per the Agreement to Sell, with the balance funded by the home loan.

Banks require: bank account statements showing fund accumulation, EPF withdrawal acknowledgment (if applicable), gift deed (if receiving money from family), fixed deposit encashment receipts, or mutual fund redemption statements. Cash deposits are scrutinized under PMLA.