City

Understanding home loan eligibility criteria before applying is essential. It determines not just whether you will get the loan, but how much, at what rate, and on what terms. Applying without checking eligibility can result in rejection, which also damages your CIBIL score.

This guide covers all eligibility parameters — for salaried employees, self-employed individuals, subsidy schemes, and top-up loans — so you can assess your eligibility and improve it before applying.

|

Parameter |

Salaried |

Self-Employed |

|

Age at Application |

21–60 years |

21–65 years |

|

Age at Loan Maturity |

Maximum 70 years |

Maximum 70 years |

|

Minimum Income |

₹25,000–30,000/month (varies by city) |

₹2.5–3 lakh net profit/year |

|

Work/Business Experience |

Min. 2 years (1 year current employer) |

Min. 3–5 years in the same business |

|

CIBIL Score |

750+ (preferred), 700+ (accepted) |

750+ preferred |

|

Loan-to-Value (LTV) |

Up to 90% (loans below ₹30 lakh) |

Up to 75–80% |

|

FOIR (obligations/income) |

Below 50–55% |

Below 50% |

|

Co-applicant |

Optional, but improves eligibility |

Often required if irregular income |

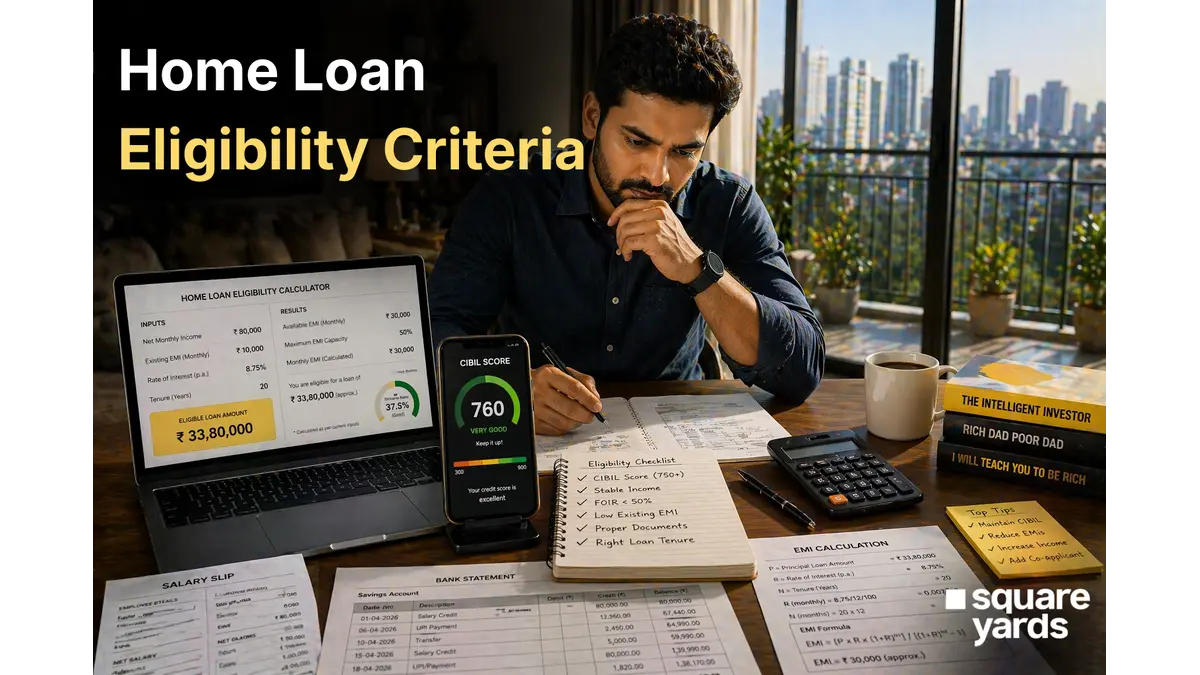

Salaried employees are the preferred borrower segment for banks due to income predictability. Key criteria:

Maximum EMI = 40–55% of Net Monthly Income

Maximum Loan Amount = Maximum EMI × Loan Factor (based on rate and tenure)

Example: Net salary ₹80,000/month, FOIR 50%, existing EMI ₹10,000:

Available EMI = ₹80,000 × 50% − ₹10,000 = ₹30,000

At 8.75% for 20 years, ₹30,000 EMI supports approximately ₹33.8 lakh loan

The Pradhan Mantri Awas Yojana (PMAY) provides interest subsidies to eligible first-time homebuyers. As of 2026, the PMAY-Urban 2.0 scheme provides subsidies to economically weaker sections and low- and middle-income groups.

|

Category |

Annual Income |

Subsidy Rate |

Max Loan for Subsidy |

Carpet Area Limit |

|

EWS (Economically Weaker Section) |

Up to ₹3 lakh |

6.5% |

₹6 lakh |

30 sq. mt. |

|

LIG (Low Income Group) |

₹3–6 lakh |

6.5% |

₹6 lakh |

60 sq. mt. |

|

MIG-I (Middle Income Group I) |

₹6–12 lakh |

4% |

₹9 lakh |

160 sq. mt. |

|

MIG-II (Middle Income Group II) |

₹12–18 lakh |

3% |

₹12 lakh |

200 sq. mt. |

Key subsidy conditions: First-time homebuyer, no existing pucca house in family, woman co-owner mandatory for EWS/LIG, property in urban areas.

A Home Loan Top-Up is an additional loan on top of your existing home loan, available to existing borrowers with a good repayment track record.

Your credit score is the single most important eligibility factor. A score of 750+ gets the best rates. Below 650, most banks will reject. Check your CIBIL score before applying and correct errors at least 6 months in advance.

Stable, verifiable income is preferred. Variable pay, commission-based income, or irregular self-employment income reduces eligibility. Adding a co-applicant with a stable income significantly boosts the loan amount.

FOIR (Fixed Obligation to Income Ratio) measures what percentage of your income already goes to loan EMIs. Lenders prefer FOIR below 50%. High existing debt — personal loans, car loans, credit card bills — directly reduces home loan eligibility.

Banks are cautious about properties over 25–30 years old (reduced tenure), properties without OC, disputed properties, and agricultural land. These factors reduce the loan-to-value ratio or lead to outright rejection.

|

Never apply to multiple lenders simultaneously — each inquiry reduces your CIBIL score by 5–10 points. Use online eligibility calculators first, then apply to 1–2 most suitable lenders. |

|

Check your home loan eligibility instantly and compare rates from 50+ lenders on SquareYards.com. Get pre-approved without impacting your CIBIL score. |

Most banks require a minimum net monthly salary of ₹25,000–30,000 in metros and ₹15,000–20,000 in smaller cities. The actual loan amount depends on income, obligations, and CIBIL score.

A CIBIL score of 750+ qualifies for the best rates and highest loan amounts. Scores between 700 and 750 are acceptable with slightly higher rates. Below 650, most banks will reject the application.

Yes — self-employed individuals can use ITR, bank statements, and business proof instead of salary slips. Some lenders also offer ‘Bank Statement’ programs for borrowers with informal income.

Yes, significantly. Adding a co-applicant (spouse, parent, sibling) with independent income increases the combined eligible loan amount. Co-applicants’ income is added to yours for calculation purposes.

PMAY-Urban 2.0 provides interest subsidies ranging from 3–6.5% for first-time homebuyers in EWS, LIG, and MIG categories. Check the official PMAY portal or your bank for the current scheme status and eligibility.

In-principle approval (eligibility assessment) takes 1–3 working days for most banks. Full sanction, including property verification, takes 7–21 working days, depending on the lender and document completeness.