Mumbai

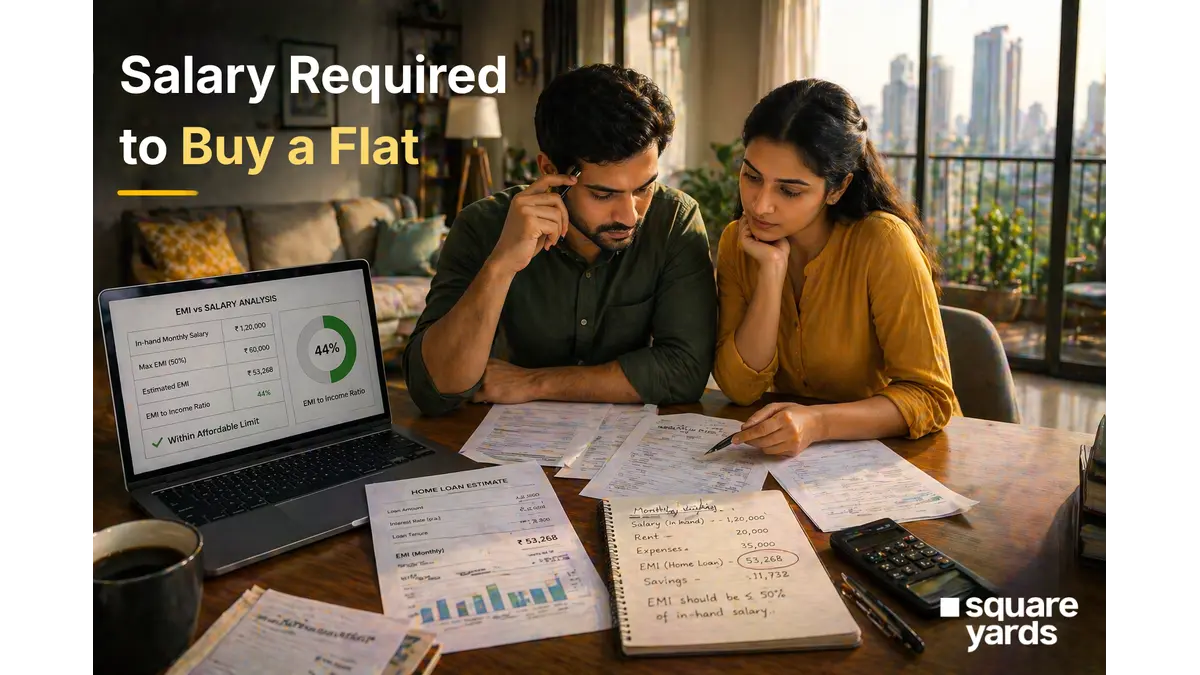

One of the most common questions from first-time homebuyers is: ‘What salary do I need to buy a flat?’ The answer depends on your city, the property price, your down payment capacity, and your existing financial obligations.

This guide breaks down the salary required to buy a flat in major Indian cities in 2026, with detailed calculations and practical benchmarks.

Two key rules determine affordability:

|

Property Value |

Loan (80%) |

EMI @ 8.75% / 20 yrs |

Min Net Salary Needed |

Min Gross Salary (approx.) |

|

₹30 lakh |

₹24 lakh |

₹21,223/month |

₹42,446–53,058 |

₹55,000–70,000 |

|

₹50 lakh |

₹40 lakh |

₹35,372/month |

₹70,744–88,430 |

₹90,000–1,10,000 |

|

₹75 lakh |

₹60 lakh |

₹53,058/month |

₹1,06,116–1,32,645 |

₹1,35,000–1,65,000 |

|

₹1 crore |

₹80 lakh |

₹70,744/month |

₹1,41,488–1,76,860 |

₹1,75,000–2,20,000 |

|

₹1.5 crore |

₹1.2 crore |

₹1,06,116/month |

₹2,12,232–2,65,290 |

₹2,60,000–3,25,000 |

|

₹2 crore |

₹1.6 crore |

₹1,41,488/month |

₹2,82,976–3,53,720 |

₹3,50,000–4,30,000 |

Assumptions: 20% down payment, 8.75% interest rate, 20-year tenure, 40–50% FOIR. No existing EMIs.

|

City |

Avg 2 BHK Price |

Salary Required (Net) |

Salary Required (Gross) |

|

Mumbai (Suburbs) |

₹1.2–1.8 crore |

₹1.8–2.7 lakh/month |

₹2.2–3.3 lakh/month |

|

Delhi (NCR) |

₹60 lakh–1.2 crore |

₹90K–1.8 lakh/month |

₹1.1–2.2 lakh/month |

|

Bengaluru |

₹80 lakh–1.5 crore |

₹1.2–2.2 lakh/month |

₹1.5–2.7 lakh/month |

|

Hyderabad |

₹60 lakh–1.2 crore |

₹90K–1.8 lakh/month |

₹1.1–2.2 lakh/month |

|

Pune |

₹60 lakh–1.1 crore |

₹90K–1.6 lakh/month |

₹1.1–2 lakh/month |

|

Chennai |

₹50 lakh–1 crore |

₹75K–1.5 lakh/month |

₹95K–1.8 lakh/month |

|

Kolkata |

₹40 lakh–75 lakh |

₹60K–1.1 lakh/month |

₹75K–1.4 lakh/month |

|

Ahmedabad |

₹35 lakh–70 lakh |

₹52K–1.05 lakh/month |

₹65K–1.3 lakh/month |

Property: ₹90 lakh 2 BHK | Down payment: ₹18 lakh | Loan: ₹72 lakh

EMI at 8.75% for 20 years = ₹63,667/month

Minimum net salary (at 50% FOIR, no other EMIs) = ₹63,667 ÷ 0.50 = ₹1,27,334/month

Approximate gross salary required: ₹1,55,000–1,70,000/month (₹18.5–20.4 lakh annually)

|

Include stamp duty (4–7%), registration (1%), GST (if under construction, 5%), and moving costs in your total budget — not just the property price and EMI. |

|

Find properties matched to your budget and salary profile across India’s top cities on SquareYards.com. Get expert guidance on affordability and loan structuring. |

For a budget flat (₹80–1 crore) in Mumbai suburbs, you need a minimum net salary of approximately ₹1.2–1.5 lakh per month (gross ₹1.5–1.8 lakh). For South Mumbai, requirements are significantly higher.

Yes, in tier-2/3 cities or affordable housing projects. A ₹50,000 net salary qualifies for approximately ₹24–28 lakh home loan (50% FOIR, no existing obligations) — enough for affordable housing in cities like Pune outskirts, Ahmedabad, or Jaipur.

The 50% EMI rule means your total monthly loan EMIs (all loans combined) should not exceed 50% of your net monthly take-home salary. This is the maximum FOIR most lenders allow.

Yes. Both salaries are combined for joint home loan eligibility. If husband earns ₹80,000 and wife earns ₹60,000 (net), combined net = ₹1,40,000, enabling EMI up to ₹56,000–70,000 per month — significantly expanding buying power.

For a 3 BHK in Delhi NCR (₹1–1.5 crore range), you need a minimum net monthly salary of ₹1.5–2.2 lakh (gross ₹1.8–2.7 lakh), assuming a standard 20-year loan and no other major obligations.