Pune

A home loan does not just help you buy your dream home — it also provides significant income tax benefits that can reduce your annual tax liability by ₹1–3 lakh or more. Yet many homebuyers either don’t fully understand these benefits or fail to claim them correctly.

This comprehensive guide covers every tax benefit on home loans in India in 2026 — for salaried, self-employed, first-time buyers, co-applicants, second home owners, and under-construction property buyers.

Note: Home loan tax benefits are available under the Old Tax Regime. If you have opted for the New Tax Regime (lower flat rates), these deductions are not available. Choose your regime wisely based on total deductions.

|

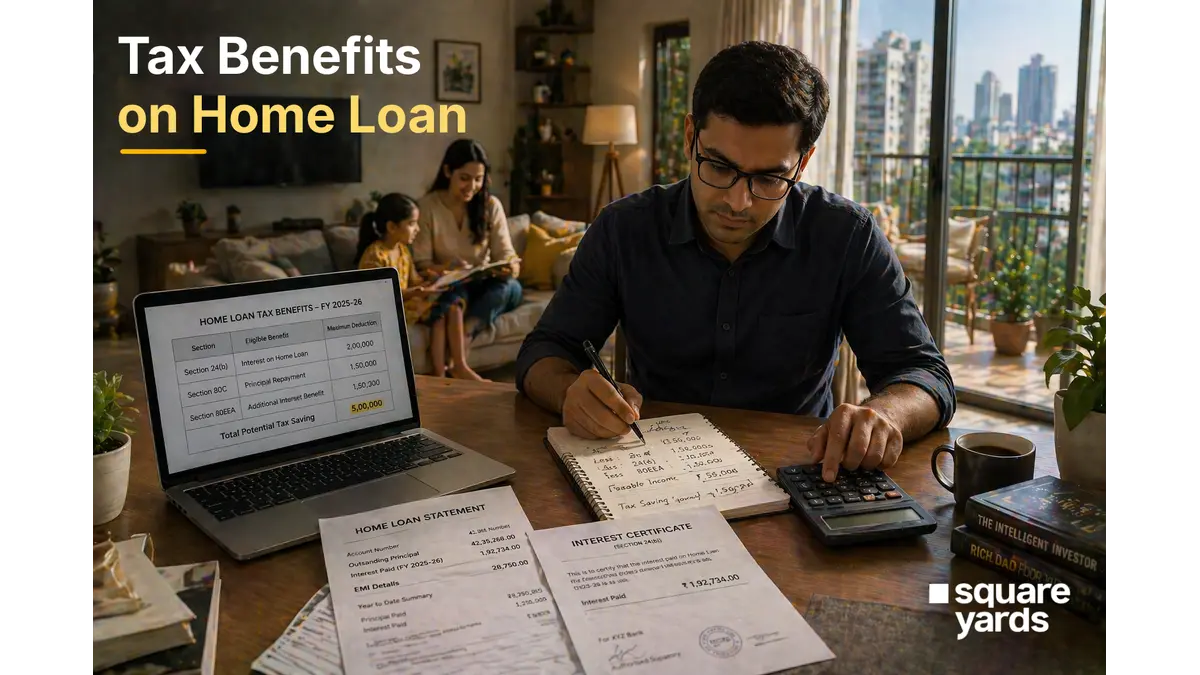

Section |

Benefit |

Maximum Deduction |

Applicable For |

|

Section 80C |

Principal repayment deduction |

₹1.5 lakh/year |

Self-occupied & let-out property |

|

Section 24(b) |

Interest on home loan deduction |

₹2 lakh/year (self-occupied) |

All home loans |

|

Section 80EE |

Additional interest benefit (first-time buyers) |

₹50,000/year |

Loans sanctioned up to March 2022 |

|

Section 80EEA |

Additional interest — affordable housing |

₹1.5 lakh/year |

Eligible first-time buyers |

|

Section 24 (let-out) |

Interest deduction on rented property |

No upper limit |

Let-out/deemed let-out property |

Section 24(b) allows deduction of interest paid on home loan from your income taxable head ‘Income from House Property’:

Principal repayment qualifies for Section 80C deduction — the same section as PPF, ELSS, LIC premium, etc. The ₹1.5 lakh limit is shared across all 80C investments.

For a first-time homebuyer under the old regime owning a self-occupied property:

|

Section |

Maximum Benefit |

At 30% Tax Slab |

|

Section 24(b) — Interest |

₹2,00,000 |

₹60,000 tax saved |

|

Section 80C — Principal |

₹1,50,000 |

₹45,000 tax saved |

|

Section 80EEA (if eligible) |

₹1,50,000 |

₹45,000 tax saved |

|

Total Maximum |

₹5,00,000 |

₹1,50,000 tax saved/year |

When a home loan is taken jointly, each co-borrower can independently claim tax benefits — provided they are also co-owners of the property:

For a second property in your portfolio, income tax treatment differs from the first home:

Yes, you can claim tax benefits on a second home loan in the same city. The second property will be treated as ‘deemed let-out’ — you pay tax on notional rent but get unlimited interest deduction.

Second home loan interest: ₹4,00,000 | Notional rent: ₹1,80,000 | Net deductible loss: ₹2,20,000 (subject to ₹2 lakh cap on set-off against other income)

Pre-construction interest (interest paid before possession) can be claimed as a deduction in 5 equal annual instalments after possession:

Section 80EEA provides an additional ₹1.5 lakh deduction on home loan interest for first-time buyers of affordable housing. As of 2026, eligibility conditions include:

|

Always declare your home loan and property ownership in your ITR, even if you do not claim deductions. Banks and tax authorities cross-check this. Non-disclosure can attract scrutiny. |

|

SquareYards’ financial advisors help you structure home loan co-ownership and tax claims optimally. Get tax-smart property advice at SquareYards.com. |

Under the old tax regime, you can claim: ₹2 lakh/year interest deduction (Section 24b), ₹1.5 lakh/year principal deduction (Section 80C), and an additional ₹1.5 lakh if eligible under Section 80EEA. Combined, this can save ₹1–1.5 lakh in annual taxes at the 30% slab.

Yes. Both co-borrowers who are also co-owners can independently claim full deductions — ₹2 lakh each under Section 24(b) and ₹1.5 lakh each under Section 80C. This doubles the total tax benefit for couples.

Yes. Interest on the second home loan is deductible under Section 24(b) without limit (since it is treated as deemed let-out). Principal repayment qualifies under 80C within the ₹1.5 lakh combined cap.

Section 24(b) allows deduction of home loan interest from income. For self-occupied property, the limit is ₹2 lakh/year. For let-out or deemed let-out property, there is no upper limit on interest deduction.

Yes. Pre-construction interest (paid before possession) is deductible in 5 equal annual instalments beginning from the year of possession, subject to the ₹2 lakh annual cap for self-occupied property.

The maximum annual interest deduction is ₹2 lakh under Section 24(b) for self-occupied property. For let-out property, there is no cap. Additionally, ₹1.5 lakh under 80EEA (if eligible) can be claimed on top.

No. Home loan deductions under Section 24(b), 80C, and 80EEA are only available under the old tax regime. If you have opted for the new tax regime, you cannot claim these deductions.

In a joint home loan where both borrowers are co-owners, each can independently claim the full Section 24(b) and 80C deductions — doubling the household tax savings. This is one of the strongest tax planning strategies for couples buying property together.