Mumbai

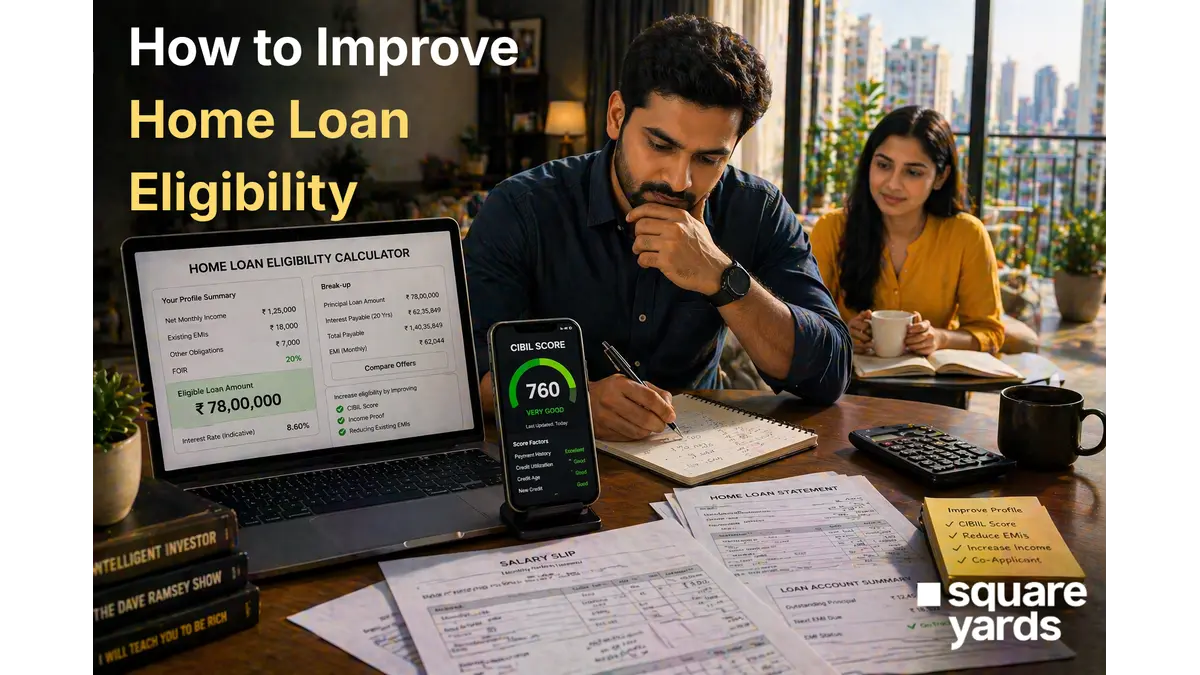

Getting home loan approval is not just about having a stable income. Banks assess dozens of parameters to determine how much loan you qualify for and at what rate. The good news: most eligibility factors are within your control and improving them can dramatically increase your loan amount and reduce your interest rate.

This guide covers the most effective, actionable strategies to improve your home loan eligibility before applying.

A higher eligible loan amount means:

Your CIBIL score directly determines approval, loan amount, and interest rate:

|

CIBIL Score Range |

Loan Approval Odds |

Interest Rate Impact |

|

800+ |

Almost certain |

Best available rate |

|

750–799 |

Very high |

Good rate |

|

700–749 |

Moderate |

0.25–0.5% higher |

|

650–699 |

Low — conditions apply |

0.5–1% higher |

|

Below 650 |

Rejection likely |

Usually rejected |

How to improve CIBIL: Pay all EMIs and credit card bills on time, reduce credit utilisation below 30%, do not close old credit cards (they improve credit history length), and correct errors in your credit report.

Adding a working spouse, parent, or sibling as a co-applicant combines both incomes for eligibility calculation. This is the fastest way to boost your eligible loan amount — often increasing it by 50–100%.

Your FOIR (Fixed Obligation to Income Ratio) — the proportion of income already going to loan EMIs — is a critical eligibility factor. Lenders allow a maximum FOIR of 50–55%. Reducing existing obligations before applying for a home loan directly increases eligibility:

Extending loan tenure from 15 to 20 years reduces your monthly EMI, which means the lender calculates a higher eligible loan amount from the same income. The trade-off is higher total interest — but higher eligibility now, with the option to prepay and close early.

Many borrowers underreport income, hurting eligibility. Lenders can consider:

Self-employed and freelance borrowers must file ITR consistently, showing stable or growing income. Banks require a minimum of 2 years of ITR — 3 years gives lenders more confidence. Avoid underreporting income in ITR as this directly caps your loan eligibility.

Different lenders have different eligibility criteria. PSU banks are strict but offer the best rates. Private banks are flexible on income documentation. NBFCs like HDFC, LIC Housing, and PNB Housing serve non-standard profiles. Matching your profile to the right lender avoids rejection and preserves your CIBIL score.

A larger down payment reduces the required loan amount. Even an extra 5% down can take you from 90% LTV to 85% LTV — making approval faster and sometimes qualifying you for better rate tiers.

Each loan application creates a ‘hard inquiry’ on your CIBIL report, reducing your score by 5–10 points. Avoid taking personal loans, car loans, or credit cards 6–12 months before your home loan application.

Banks offer better eligibility and sometimes lower rates to customers who maintain their primary salary account. It also reduces documentation requirements and speeds up processing.

Properties with a clear title, valid OC, RERA registration, and from reputed builders receive higher LTVs and faster approvals. Avoid properties with title disputes, no OC, or in non-notified areas.

If existing high-cost loans reduce your FOIR, balance-transfer them to lower-rate products first. This reduces your existing EMI obligations, freeing up capacity for the new home loan.

CIBIL reports contain errors for approximately 20–25% of consumers (e.g., incorrect closed loans defaults). Check your free annual CIBIL report and dispute errors — corrections can improve your score by 30–50 points.

Banks look favourably at borrowers with consistent savings — regular SIP, FD, or savings account deposits demonstrate financial discipline. A 6–12-month savings history before application strengthens your profile.

Changing jobs within 3–6 months of application reduces lender confidence in income stability. Lenders prefer at least 1 year with the current employer. If you must change jobs, wait until the loan is disbursed.

|

Start improving CIBIL and reducing obligations at least 6–12 months before your planned home loan application. Last-minute fixes rarely move the needle significantly. |

|

SquareYards’ home loan team helps you identify the right lender for your profile and improve eligibility before applying. Get personalised guidance at SquareYards.com. |

The fastest improvements come from adding a high-income co-applicant, closing high-cost personal loans to reduce FOIR, and correcting CIBIL report errors. These can show results within 3–6 months.

Yes. A longer tenure reduces the required monthly EMI for the same loan amount, effectively increasing the maximum loan the lender will sanction. A 20-year tenure qualifies for a 15–20% higher loan than a 15-year tenure.

Some NBFCs and private lenders may consider borrowers with a 650 CIBIL score, but at higher interest rates and lower LTV. PSU banks typically require 700+ and ideally 750+. It is better to improve the score before applying.

A co-applicant with poor CIBIL can actually hurt your application — lenders evaluate the CIBIL of all applicants. Only add co-applicants with 700+ CIBIL scores.

Most banks require 3–6 months’ salary slips. Along with Form 16, the last 6 months’ bank statements, and the latest 2 years’ ITR for a complete income assessment.