The Gratuity Act, the Payment of Gratuity Act, 1972, was designed to ensure employees receive a token of appreciation for their continuous service in an organization. The gratuity amount is a one-time payment. Therefore, the workers receive it either after their retirement or after at least five years of consistent service in a specific company.

A few years ago, the gratuity payment was limited to ₹ 10 lakh, above which the employee had to pay the required tax. However, after the new amendment in the Act (some may call it as Gratuity Act 2020), the threshold limit increased to ₹ 20 lakh.

Sounds interesting. Right? Well, keep reading, and it will get better and more knowledgeable.

We have covered the content of various Sections in the Gratuity Act, its main objectives, advantages, and more! So, stay with us until the end.

Let us begin with the definition of the Payment of Gratuity Act, 1972.

What is Payment of Gratuity?

The Payment of Gratuity is an act known as the ‘Payment of Gratuity Act, 1972. It ensures that industries and organizations pay a one-time gratuity to their employees after completing a specific period.

The law applies to factories, railways, shops, oilfields, ports, and mines. The gratuity amount refers to the fifteen days’ wages for every year of employee services subject to a maximum of ₹ 20 lakhs.

In the case of contracts or seasonal establishments, the payable gratuity depends on the rate of seven days’ wages for each season. The Act doesn’t impair the right of an employee from receiving better terms of gratuity under any contract or agreement or award with the employer.

Central Government is the appropriate regulatory concerning an institution pertaining to or under the control of the Central Government or holding branches in more than one state or an institution of a factory pertaining to or under the control of Central Government or of an oilfield railway, major port, or mine.

Rules of Gratuity Act, 1972

Gratuity rules are as follows:

- According to Gratuity Act, a company with ten or more employees must pay a gratuity amount to its workers.

- To receive gratuity, the employee must complete a minimum of five years of tenure with the same organization.

- Employees can get the gratuity only in the following conditions:

- Resignation

- Retirement

- Disablement due to a disease or accident

- VRS

- Termination

- Lay off because of retrenchment.

- The gratuity estimation depends solely on the employee’s last drawn basic salary plus the dearness allowance.

- If an employee is terminated because of his involvement in an offense concerning moral turpitude, riotous conduct, or any other violent act, his gratuity will be forfeited.

- Employers must pay their employees the gratuity, regardless of they have gone bankrupt.

- A gratuity fund of up to ₹ 20 lakh has got an exemption from taxes.

- The tax on gratuity amount differs from different organizations.

- Gratuity payment to the legal heir or widow of an employee will be qualified for tax exemption.

- The tax exemption for the threshold of ₹ 20 lakh is for cumulative gratuity received. For instance, Khushboo worked continuously with an organization for 20 years and got a gratuity of ₹ 19 lakh.

She joined another company, and after seven years of service, she received a gratuity of ₹ 5 lakhs. In total, she has a gratuity of ₹ 24 lakhs. Hence, as per the act, she will have to pay a tax of ₹ 4 lakh to the government.

So, this was just a little glance at what’s in there in the Payment of Gratuity Act, 1972. Now, let me take you on a long tour of the payment of gratuity rules.

What is Section 1 of the Gratuity Act?

Section 1 of the Gratuity Act defines the title, extent, application, and commencement.

- The act is known as the Payment of Gratuity Act, 1972.

- It applies to the whole of India

Provided: As it relates to ports and plantations, it must not stretch to Jammu and Kashmir.

- It must apply to –

a) All the factories, oilfields, ports, plantations, mines, and railway companies.

b) All the establishments and shops within the application of any law for the time being in force concerning establishments and shops in a State, where ten or more employees are employed or were employed, on any day of the preceding year;

c) Other such establishments or their classes have employed ten or more than ten employees or any day of the next twelve months, as specified by the Central Government on this behalf.

3 (A) An establishment or shop to which this Act applies must continue to be governed by this Act. Nevertheless, the number of people hired therein at any time after it has got so applicable goes below ten.

- The Act may come into force on the date as notified by the Central Government.

What is Section 2 of the Payment of Gratuity Act, 1972?

Section 2 of the Gratuity Act clarifies the definitions. In this Act, unless the context otherwise demands,-

a) “appropriate Government” means-

(i) concerning an establishment

(a) under the control of or belonging to, the Central Government,

(b) holding branches in more than one State,

(c) of a factory under the control of, belonging to, the Central Government,

(d) of a major oilfield, port, railway company, or mine, the Central Government,

(ii) in any other instance, the State Government;

(b) “completed year of service” refers to constant service for one year;

[2] [(c) “continuous service” refers to consistent service as specified in section 2A;](d) “controlling authority” means an authority delegated by the appropriate Government under section 3 ;

(e) “employee” refers to any person (other than an apprentice) employed on wages, [3] in any factory, establishment, mine, plantation, oilfield, railway company, port, or shop, to do any skilled, semi-skilled, or unskilled, manual, technical, supervisory, or administrative work, whether the terms of such employment are implied or express, [4] [and whether or not such person is working in an administrative or managerial capacity, but doesn’t include any such person holding a post under the State or Central Government and is regulated by any other Act or by any rules offering gratuity payment].

(f) “employer” refers to, concerning any plantation, port, factory, mine, railway company, oilfield, establishment, or shop –

(i) under the control of or belonging to, the State or Central Government, a person or authority elected by the appropriate Government for the control and supervision of employees, or where no person or authority has been so elected, the head of the Ministry or the Department concerned,

(ii) under the control of or belonging to, any local authority, the person elected by such authority for the control and supervision of employees or where no person has been so designated, the chief executive officer of the local authority,

(iii) in any other case, the person who, or the authority which, has the ultimate control over the activities of the railway company, factory, mine, plantation, oilfield, port, establishment or shop, and where the said activities are consigned to any other person, whether called a manager, managing director or by any other name, such person;

(g) “factory” has the meaning-assigned to it in clause (m) of section 2 of the Factories Act, 1948 (63 of 1948);

(h) “family”, concerning an employee, shall be deemed to consist of –

(i) in the case of a male employee, himself, his wife, and his children, whether married or unmarried, his dependent parents

[6] [and the dependent parents of his wife and the widow] and children of his predeceased son, if any,(ii) in the case of a female employee, herself, her husband and children, whether married or unmarried, her dependent parents and the dependent parents of her husband and the widow and children of her predeceased son, if any:

(i) The meaning of “major port” is attributed to it in clause (8) of section 3 of the Indian Ports Act, 1908;

(j) The definition of “mine” is attributed to it in clause (J) of sub-section (1) of section 2 of the Mines Act, 1952;

(k) “notification” refers to a notification issued in the Official Gazette;

(l) The definition of “oilfield” has been attributed in clause (e) of section 3 of the Oilfields (Regulation and Development) Act, 1948;

(m) The meaning of “plantation” has been attributed in clause (f) of section 2 of the Plantations Labour Act, 1951;

(n) The meaning of “port” has been attributed in clause (4) of section 3 of the Indian Ports Act, 1908;

(o) “prescribed” means specified by rules framed under this Act;

(p) “railway company” has the meaning assigned to it in clause (5) of section 3 of the Indian Railways Act, 1890;

(q) “retirement” refers to the termination of an employee’s service otherwise than on superannuation;

[8] [(r) “superannuation”, concerning an employee, refers to the employee’s attainment of such age as is set in the service’ contract or conditions at the age on the attainment of which the employee will leave the employment;](s) “wages” refers to all emoluments that an employee warns during the duty or while on leave following the terms and conditions of his employment. Also, some are paid or are payable to him in cash and comprise dearness allowance but do not include any bonus, overtime wages, house rent allowance, commission, and any other allowance.

Section 2A of the Act- Continuous Service

For the purposes of this Act, –

(1) an employee shall be said to be in continuous service for a period if he has, for that period, been in uninterrupted service, including service which may be interrupted on account of sickness, accident, leave, absence from duty without leave (not being absent in respect of which an order [***] treating the absence as a break in service has been passed in accordance with the standing order, rules or regulations governing the employees of the establishment), lay off, strike or a lock-out or cessation of work not due to any fault of the employee, whether such uninterrupted or interrupted service was rendered before or after the commencement of this Act.

(2) where an employee (not being an employee employed in a seasonal establishment) is not in continuous service within the meaning of clause (1), for any period of one year or six months, he shall be deemed to be in continuous service under the employer –

(a) for the said period of one year, if the employee during the period of twelve calendar months preceding the date with reference to which the calculation is to be made, has actually worked under the employer for not less than –

(i) one hundred and ninety days, in the case of an employee employed below the ground in a mine or in an establishment that works for less than six days in a week; and

(ii) two hundred and forty days, in any other case;

(b) for the said period of six months, if the employee during the period of six calendar months preceding the date with reference to which the calculation is to be made has actually worked under the employer for not less than –

(i) ninety-five days, in the case of an employee employed below the ground in a mine or in an establishment that works for less than six days in a week; and

(ii) one hundred and twenty days, in any other case;

Explanation: For the purpose of clause (2), the number of days on which an employee has actually worked under an employer shall include the days on which –

(i) he has been laid-off under an agreement or as permitted by standing orders made under the Industrial Employment (Standing Orders) Act, 1946

(20 of 1946), or under the Industrial Disputes Act, 1947 (14 of 1947), or under any other law applicab1c to the establishment;

(ii) he has been on leave with full wages, earned in the previous year;

(iii) he has been absent due to temporary disablement caused by an accident arising out of and in the course of his employment and

(iv) If it’s a female who has been on maternity leave; so, however, that the total period

in the case of a female, she has been on maternity leave; so, however, that the total period of such maternity leave does not exceed twelve weeks.

(3) where an employee working in a seasonal establishment, isn’t serving continuously within the definition of clause (1), for any period of six months or one year, he must be deemed to continue the service under the employer for the said period if he has been really employed for not less than seventy-five percent of the number of days on which the establishment was in operation at that time.

Section 3 of the Gratuity Act, 1972- Controlling Authority

Section 3 of the Payment of Gratuity Act, 1972 defined that-

The appropriate Government may appoint any officer, by notification, to become the controlling authority. The authority must be accountable for the enforcement of this Act, and there would be different controlling authorities for different areas.

Section 4: Payment of Gratuity

(1) An employee shall receive gratuity on the termination of his employment after he had dedicated consistent service to the organization for not less than five years,-

- on his resignation or retirement

- on his superannuation, or

- on his disablement or death due to disease or accident:

Provided: The completion of consistent service of five years shall not be required where the employment termination of any employee is due to disablement or death:

Provided further: If the employee dies, the employer must pay the gratuity payable to him to his nominee. In case the employee hasn’t made any nomination to his heirs, and where the heir is minor, then his shares must be submitted with the controlling authority. The authority will further invest the same for the benefit of the minor in banks or other financial institutions, as may be specified until the minor attains majority.

The section further continues and defines various situations and manners in which the gratuity amount will be payable and not payable to employees.

To know more about this Section, you can visit the official website of the Chief Labour Commissioner (Central) and read the regulations.

Section 4 A – Insurance

Section 4 (A) of the Gratuity Act states the following:

(1) With effect from dates as notified by the appropriate Government on this behalf, every employer, other than an employer or an establishment under the control of or belonging to, the State or Central Government, shall subject to the provisions of sub-section (2), get insurance in a specified manner, from the LIC India established under the Life Insurance Corporation of India Act, 1956 (31 of 1956) or any other specified insurer:

Provided: Different dates may be elected for distinct establishments or their classes or diverse areas.

(2) The appropriate Government may, subject to such conditions as may be specified, exempt all the employers who had already established approved gratuity money for their employees and who wish to continue such arrangement and every employer employing five hundred or more employees who establish approved gratuity money in the specified for form the provisions of sub-section (1).

(3) To effectively implement the provisions of this section, all employers must get their establishments registered within the prescribed time with the controlling authority in a specified manner. Further, no employer should be registered under the provisions of this Section unless he has got insurance defined in sub-section (1) or has established an approved gratuity fund referred to in sub-section (2).

(4) The appropriate Government may set rules to give effect to the provisions of this Section. Further, such rules may offer the composition of the Board of Trustees of the approved gratuity fund and for the recovery by the controlling authority of the gratuity amount for the employee from LIC or any other insurer with whom insurance is availed of under sub-section (1), or the Board of Trustees of the approved gratuity fund, as the case may be.

(5) Where an employer fails to pay through premium to the insurance referred to in sub-section (1) or through contribution to all approved gratuity funds described in subsection (2), he shall be accountable to pay the due gratuity fund under this Act (including interest, if any, for delayed payments) directly to the controlling authority.

(6) Whoever violates the provision of sub-section (5) will be punishable with a penalty which may stretch to ten thousand rupees. If the offense continues, an additional fine of one thousand rupees may extend for each day while the offense continues.

Explanation: In this section “approved gratuity fund” will mean the same as in clause (5) of section 2 of the Income Tax Act, 1961.

Section 5 – Power to Exempt

As the title suggests, Section 5 deals with the power to exempt. It states the following:

(1) The appropriate Government may exempt any factory, establishment, oilfields, mines, ports, shops, or railway company to which the Act is applicable from the operation of the provisions of this Act if the Government finds the aforementioned establishments will get the gratuity or pensionary advantages not less favorable than the benefits defined under this Act.

(2) The appropriate Government may exempt any employee/ class of employees working in a factory, establishment, oilfields, mines, ports, shops, or railway company to which the Act is applicable from the operation of the provisions of this Act if the Government finds that such employees or their class will get the gratuity or pensionary advantages not less favorable than the benefits defined under this Act.

(3) A notification issued under sub-section (1) or (2) may be issued a date, not before the date of commencement of this Act. However, no such notification will be issued that can impair any person’s interest prejudicially.

Section 6 – Nomination

The Section states the following:

- Every employee who has completed one year must nominate within the prescribed time, form, and manner for the second proviso to sub-section (1) of Section 4.

- In the nomination, the employee may distribute the gratuity amount to be paid to him under this Act amongst more than one nominee.

- If the employee has a family while he is nominating, he must nominate one or more family members. Further, any nomination created by the employee in favor of a person who isn’t a family must be void.

- While nomination, if the employee doesn’t have any family, he can nominate any person/persons. However, if the employee acquires a family afterward, such nomination will forthwith be invalid. Moreover, the employee must make an afresh nomination in favor of his new family within the prescribed time.

- An employee can modify the nomination at any time, subject to the provisions of sub-sections (3) after sending a written notice to his employer in such manner and form as may be prescribed of his intention behind the same.

- If the nominee dies before the employee, the employee must make an afresh nomination in the prescribed form concerning such interest.

- The employee must send all the nominations, including fresh or altered, to his employer, who must keep them in his safe custody.

Section 7 – Determination of the Amount of Gratuity

Section 7 of the Act defines how to determine the gratuity amount.

- A person eligible for receiving a gratuity under this Act or any authorized person, in writing, to receive on his behalf shall write an application to the employer, within such form and time, as may be instructed, for such gratuity payment.

- As soon as an employee becomes eligible to receive gratuity, the employer shall, whether an application indicated in sub-section (1) has been made or not, determine the gratuity amount and notify the person receiving gratuity and the controlling authority specifying the gratuity amount so estimated in writing.

- The employer shall pay the gratuity within thirty days from the date employee becomes eligible for the payment.

3 (A) If the employer doesn’t pay the gratuity amount payable under sub-section (3) within the specified period in sub-section (3), the employer shall pay simple interest from the date on which gratuity gets payable, at rates not exceeding the one defined by the Central Government from time to time for the repayment of long-term deposits, as the Government may specify by notification:

Provided: the employer won’t pay any such interest if the delay in payment is the employee’s fault and the employer has the written consent from the controlling authority for the same.

- 4 (A) In case of any conflict concerning the payable gratuity amount to an employee under this Act or an employee for payment of gratuity or as to the admissibility of any claim or, or as to the individual receiving the gratuity, the employer must deposit the amount to the controlling authority as he agrees to be payable by him as gratuity.

(b) Where there’s any disagreement related to any matter/matters defined in clause (a), the employee or employer or any other person creating the conflict may send an application to the controlling authority to decide the dispute.

(c) After the inquiry and after the parties to the dispute have received a fair opportunity of being heard, the controlling authority must identify the matter/matters in conflict. If, as a consequence, the employee should get the payable amount, the controlling authority will instruct the employer to pay the amount, or as the case may be, the already deposited amount would be reduced from the payable amount.

(d) The controlling authority must pay the amount deposited along with the excess amount if the employer has deposited it to the person receiving it.

(e) If the employer has deposited the amount as under clause (a), the authority must pay the deposit amount to the applicant where he works. In another case, the amount should be paid to the applicant who isn’t the employee i.e to the nominee, the guardian of the nominee, or heir of the employee, if the authority finds no dispute associated with the right of the applicant receiving the gratuity amount.

- To conduct an inquiry under sub-section (4), the authority must hold the powers as vested in a court, while examining a suit under the Code of Civil Procedure, 1908 (5 of 1908), in respect of the matters as follows:

(a) Examing any person’s attendance or enforcing him on oath;

(b) Claiming the production and discovery of documents;

(c) Getting data on affidavits;

(d) Issuing commission for investigating the witnesses.

- Any inquiry under this Section must be a legal proceeding with the meaning of Sections 193 and 228, and to serve Section 196, of the Indian Penal Code, 1860 (45 of 1860).

- An order aggrieving any person under sub-section (4) may appeal to the appropriate Government or any such concerned authority as specified by the controlling Government in this regard within sixty days from the date of receiving the order:

Provided: The appellate authority or the concerned Government is convinced that the appellant was prevented by enough causes from favoring the appeal within sixty days, stretching the said period by sixty days further.

Provided: No further appeal by an employer will be submitted during the appeal unless the appellant either presents a certificate to the controlling authority with the effect that it has paid him the amount equal to the gratuity money needed to be submitted under sub-section (4), or deposits with the appellate authority the amount.

- The appellate authority or the concerned Government may confirm, modify or reverse the controlling authority’s decision after offering the parties to the appeal a fair opportunity.

Section 7 A – Inspectors

As it’s pretty evident from the above sub-head, Section 7 A of the Gratuity Act deals with the inspector. It states that-

- By notification, the appropriate Government may appoint as many Inspectors as it deems fit to serve the goals of this Act.

- As per general or special order, the regulatory authority may define the extent to which the jurisdiction of an Inspector shall extend. It also refers to the area where two or more Inspectors shall be appointed for the same place, also render, by such order, for the allocation or distribution of work to be done by them under the said Act.

- All the inspectors shall be considered public servants within the meaning of Section 21 of the Indian Penal Code, 1860 (45 of 1860).

Main Objective of the Gratuity Act

The prime objective of this act is to aid financial support to employees by offering them gratuity after they retire. It is to recognize their consistent, exemplary services and sincere efforts towards the organization by the employee.

Don’t Miss Out

Advantage of Gratuity Act

The gratuity act was established to render various benefits. Some of them are as follows:

1) Every employee of the company with ten or more employees receives a one-time payment as a token of appreciation for their continuous service of at least five years in the organization.

2) Even if the company goes bankrupt, it is bound to pay the gratuity amount to its employees.

3) Gratuity isn’t completely exempted from tax. You must consider the maximum limit as any amount beyond ₹ 20 lakh will not be exempted from tax.

4) In case you plan to change your organization before five years, you must reconsider as you might miss out on a huge amount.

5) You can also nominate your family members for the gratuity amount by filling ‘Form-F’ while joining.

Frequently Asked Questions (FAQs)

Q1. What is the Payment of Gratuity Act 1972?

Ans: The law applies to factories, railways, shops, oilfields, ports, and mines. The gratuity amount refers to the fifteen days’ wages for every year of employee services subject to a maximum of ₹ 20 lakhs.

Q2. What is the main purpose of the Gratuity Act?

Ans: The main purpose of establishing the Gratuity Act is to ensure every company or organization with more than 10 employees or those covered in the Gratuity Act, pays a one-time gratuity to their employees after completing a specific period or after their retirement.

Q3. What is the rule for payment of gratuity?

Ans: Gratuity rules are as follows:

- According to Gratuity Act, a company with ten or more employees must pay a gratuity amount to its workers.

- To receive gratuity, the employee must complete a minimum of five years of tenure with the same organization.

- Employees can get the gratuity only in the following conditions:

- Resignation

- Retirement

- Disablement due to a disease or accident

- VRS

- Termination

- Lay off because of retrenchment.

- The gratuity estimation depends solely on the employee’s last drawn basic salary plus the dearness allowance.

- If an employee is terminated because of his involvement in an offense concerning moral turpitude, riotous conduct, or any other violent act, his gratuity will be forfeited.

- Employers must pay their employees the gratuity, regardless of they have gone bankrupt.

- A gratuity fund of up to ₹ 20 lakh has got an exemption from taxes.

- The tax on gratuity amount differs from different organizations.

- Gratuity payment to the legal heir or widow of an employee will be qualified for tax exemption.

- The tax exemption for the threshold of ₹ 20 lakh is for cumulative gratuity received. For instance, Khushboo worked continuously with an organization for 20 years and got a gratuity of ₹ 19 lakh.

She joined another company, and after seven years of service, she received a gratuity of ₹ 5 lakhs. In total, she has a gratuity of ₹ 24 lakhs. Hence, as per the act, she will have to pay a tax of ₹ 4 lakh to the government.

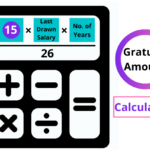

Q4. How is the payment of the Gratuity Act 1972 calculated?

Ans: To calculate the Gratuity, follow the following formula:

The formula is: (15 * Your last drawn salary * the working tenure) / 30.

For example: You have worked with a company continuously for 8 years and your last basic salary drawn was ₹ 80,000. Therefore, you will get a gratuity of-

Gratuity = ₹ 15 x 80,000 x 8/30 = ₹ 3,20,000. Hence, you will receive the gratuity of ₹ 3,20,000.